The Financial Imperative of HTS Precision in 2026 Trade Compliance

Why HTS classification accuracy now directly determines COGS, EBITDA stability, and False Claims Act exposure in the 2026 trade enforcement environment.

Chansam Kim

January 8, 2026

The Financial Imperative of HTS Precision: A Quantitative and Legal Analysis of Trade Compliance in the 2026 Fiscal Landscape

The global trade ecosystem is currently navigating a period of unprecedented complexity, where the intersection of shifting geopolitical alliances, high-frequency regulatory updates, and aggressive enforcement by Customs and Border Protection (CBP) has elevated the role of the Harmonized Tariff Schedule (HTS) to a critical financial priority. For the modern Chief Financial Officer (CFO) and trade manager, the HTS code is no longer a mere clerical identifier for logistics; it is a fundamental driver of the Cost of Goods Sold (COGS), a primary determinant of EBITDA stability, and the front line of defense against the Department of Justice (DOJ) and False Claims Act (FCA) litigation. In fiscal year 2024 alone, U.S. Customs and Border Protection processed 38.3 million entry summaries with a total value of $3.36 trillion, illustrating the massive scale of exposure for companies that treat classification as a routine back-office task.

The financial architecture of a corporation relies on the predictability of its margins, yet this predictability is frequently undermined by the "compliance shadow", the gap between a company’s active catalog and its legally defensible classification data. Most enterprise-scale importers maintain catalogs with thousands or tens of thousands of Stock Keeping Units (SKUs), yet manual processes often limit review coverage to a mere 15% of the total inventory. This leaves 85% of a company’s trade operations at risk of being triggered by one of the 2,000+ regulatory changes that occur annually. When these risks materialize, the result is often a multi-million dollar settlement that reflects not just the missing duties, but the accumulated weight of years of non-compliance, legal fees, and statutory penalties.

The Taxonomy of Misclassification and Its Financial Consequences

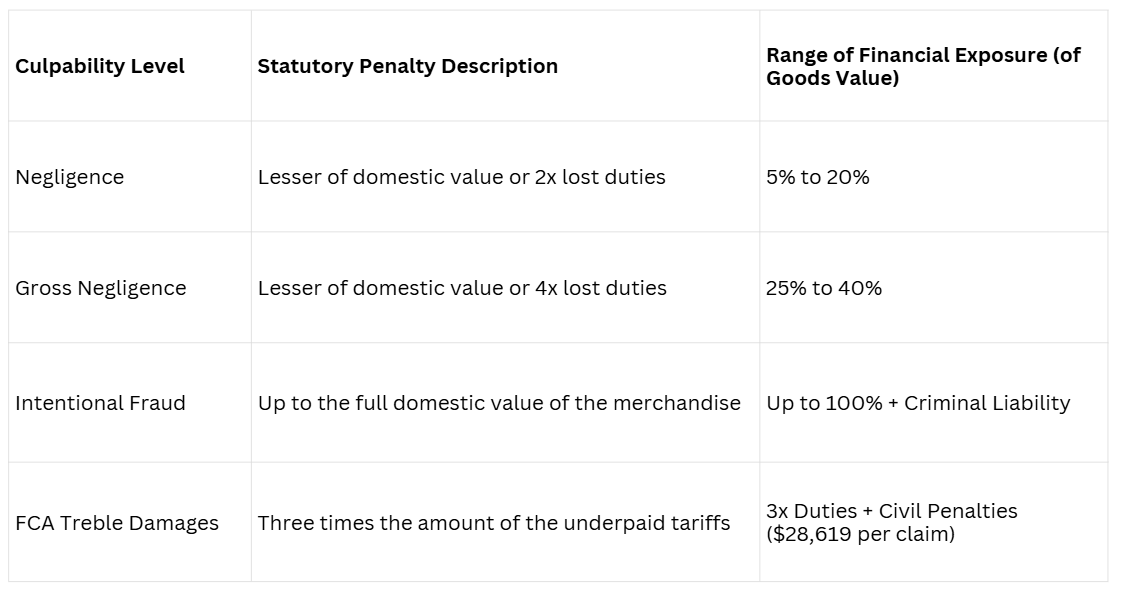

The financial impact of misclassification is structured by the degree of culpability and the specific trade statutes applied. Enforcement has shifted toward the use of sophisticated data analytics and algorithmic monitoring to identify statistical anomalies in import pricing and HTS coding patterns. When an anomaly is detected, the ensuing investigation examines whether the importer exercised "reasonable care" as required by 19 U.S.C. 1484.10 The failure to do so results in a hierarchy of penalties that can significantly exceed the domestic value of the merchandise in question.

Penalty Structures Under U.S. Customs Law

The following table delineates the financial exposure associated with different levels of compliance failure. These percentages apply to the value of the merchandise, highlighting how a single technical error can compound into a catastrophic financial event.

The introduction of Section 301 tariffs, which add up to 25% (and in some 2026 scenarios, even higher reciprocal rates) to Chinese-origin goods, has drastically increased the "incentive" for misclassification, which in turn has sharpened the focus of government investigators. For an importer with $10 million in annual volume, a negligent misclassification of goods previously subject to a 0% rate but now subject to a 25% Section 301 rate results in a base duty loss of $2.5 million. Once the statutory penalties and interest are applied, the total settlement could easily reach $5 million to $7 million for a single year of imports.

Forensic Analysis of Key HTS Misclassification Case Studies

To understand the operational mechanisms that lead to these financial failures, one must examine the specific patterns of behavior revealed in recent federal settlements. These cases demonstrate that the primary risk is not just the initial error, but the persistence of that error after internal or external warnings have been issued.

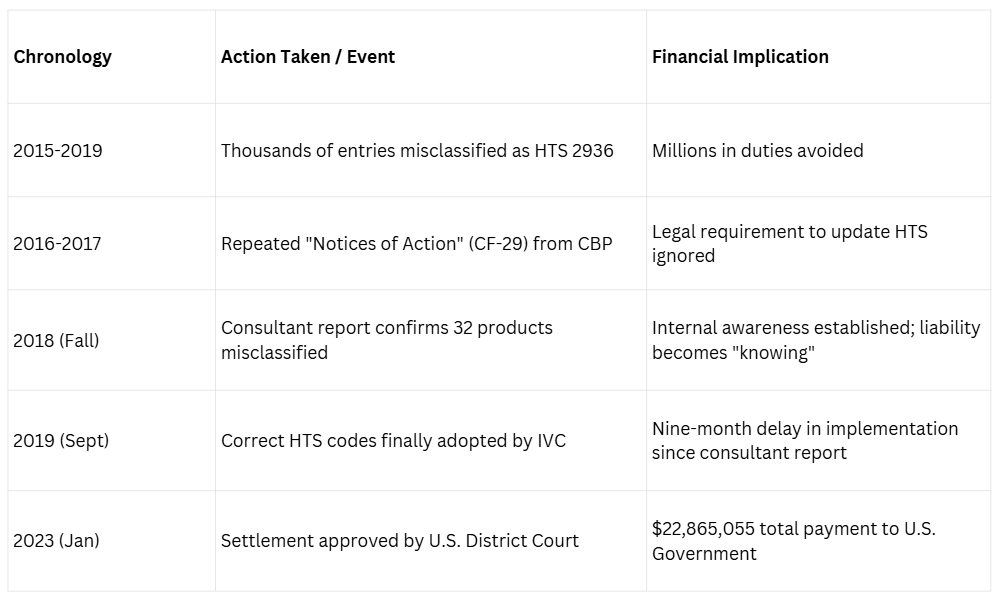

Case Study: Escalation of HTS Classification Errors into Corporate Liability

A major U.S. enforcement action finalized in early 2023, resulting in a $22.8 million settlement, provides a clear illustration of how HTS classification failures can escalate from technical errors into enterprise-level legal and financial crises.

Technical Mechanism of Failure

The case involved a multi-year pattern of misclassification related to vitamins and nutritional supplements imported from China. The core technical issue centered on the distinction between pure chemical compounds and food preparations. The importer consistently classified the products under HTS Heading 2936, which applies to pure vitamins and carries a duty-free rate. However, the imported goods were vitamins in dosage form or combined as dietary supplements, which required classification under HTS Heading 2106.90., a provision subject to materially higher duties.

The financial progression of this enforcement action is summarized in the table below.

What makes this case particularly instructive for finance and compliance leaders is the role of internal documentation. Investigators identified internal communications acknowledging awareness of the classification issue, including statements recognizing the difficulty of remediation. Despite this knowledge, the importer did not remit back-duties for prior entries. This failure to self-disclose after gaining awareness converted a technical classification error into a violation under the False Claims Act, triggering treble damages and restitution totaling more than $22.8 million.

Material Misrepresentation in Industrial Imports

A separate enforcement action, resulting in a $22.2 million settlement, highlights the risks associated with material-based misclassification in industrial goods. In this case, an international engineering and manufacturing enterprise misrepresented the composition of pipe products imported from China. Stainless steel products, subject to significant anti-dumping and countervailing duties (AD/CVD), were declared as carbon steel, which carries substantially lower duty rates.

This case illustrates a “first-order” balance sheet impact of misclassification. The avoidance of AD/CVD duties, which can equal or exceed 100% of the merchandise value, led to an artificial inflation of operating margins. When enforcement authorities intervened, the settlement effectively reversed those unearned margins and imposed additional penalties, resulting in a sudden, unforecasted reduction in EBITDA.

The Technicality of Surface Area in Footwear Classification

Footwear remains one of the most technically complex areas of the HTS, with duty rates determined in part by the “External Surface Area of the Upper” (ESAU). In one enforcement matter, an importer incurred a $1.6 million penalty after incorrectly classifying footwear as rubber tennis shoes.

This case demonstrates how a single technical misinterpretation, often reduced to one digit in the HTS code, can compound into tens of millions of dollars in cumulative liability over time. For trade and compliance managers, the lesson is clear: marketing descriptions are legally irrelevant. Customs classification is governed exclusively by physical characteristics and material composition, and those technical determinations directly define financial exposure.

Accounting for Trade Risk: GAAP, COGS, and Inventory Valuation

For the CFO, the impact of HTS classification extends into the core of financial reporting. Under Generally Accepted Accounting Principles (GAAP), specifically FASB ASC 330, tariffs are treated as inventoriable costs. This means they are capitalized as part of the total cost of the asset on the balance sheet and only recognized as an expense (COGS) when the inventory is sold.

The Impact on EBITDA and Margin Reporting

The relationship between HTS accuracy and financial reporting can be modeled using the standard inventory cost equation:

If a trade manager uses a 0% duty code for an item that should be 25%, the inventory asset is undervalued by 25% of the import price. When the error is caught, the following financial disruptions occur:

Sudden Margin Compression: The retroactive application of duties creates a massive, unplanned increase in COGS for the current period, leading to a direct hit to gross profit and EBITDA.

Net Realizable Value (NRV) Write-Downs: If the new duty-inclusive cost of the inventory exceeds the price for which it can be sold, the company must write down the inventory to its NRV under ASC 330-10-35-1B. Once a write-down occurs, the new cost basis is permanent, even if market conditions improve.

Liquidity Strain: CBP requires the payment of duties at the time of entry. A discovery of misclassification leads to "liquidated damages," where the company must come up with cash for back-duties and interest immediately, often straining working capital.

Operational Vulnerabilities in Manual Classification Systems

The persistent nature of HTS errors is rooted in the "daily reality" of trade compliance teams who are overwhelmed by the volume of data. Manual review of a single SKU takes approximately 45 minutes. For a retailer or industrial distributor with 20,000 SKUs, a full re-classification effort would require 15,000 man-hours, roughly the work of 7.5 full-time employees for an entire year, just to handle one round of regulatory changes.

The Efficiency Gap and Its Financial Correlation

Because manual review is impossible at scale, most companies rely on "sampling" or "tribal knowledge" from customs brokers. This creates several operational vulnerabilities that have direct financial correlations:

Catalog Stale-ness: When HTS codes change (as they do 2,000+ times per year), the "stale" codes remain in the ERP system, triggering incorrect duty payments on every subsequent shipment.

Response Latency: A CF-28 request for information from CBP typically takes 3-4 weeks to answer manually, as teams scramble to find the "evidence chain" for the original classification. This delay often leads to shipment holds and demurrage costs.

Inconsistent Reasoning: Different brokers or employees may classify the same product differently across various ports of entry, creating the statistical anomalies that CBP’s algorithms are designed to catch.

The product SAIL GTX was developed by the company SAIL specifically to address these structural failures by transforming classification from a manual, error-prone task into an AI-native, defensible financial strategy.

Transitioning to Defensible Trade Operations with SAIL GTX

The objective of SAIL GTX is to provide a workspace where HTS classification, tariff stacking, and audit defense happen simultaneously. By moving from a "guess-and-check" model to an "evidence-first" model, companies can achieve a level of precision that matches the investigative capabilities of federal agencies.

Features of an AI-Native Trade Compliance Ecosystem

SAIL introduces several features that directly mitigate the financial risks identified in the above cases:

Reasoning and Evidence Chains: Unlike basic automation tools that simply provide a 10-digit code, SAIL GTX provides the legal reasoning, citations from the CROSS ruling database, and confidence scores for every decision. This creates a "defensible position" that can be exported as documentation for prior disclosure or audit response.

Continuous Regulatory Monitoring: SAIL GTX engine checks the entire product catalog against global regulatory changes daily. When a code is updated or a new Section 301 list is published, the system flags the affected SKUs immediately, preventing the "stale classification" risk that led to the $22.8 million failure case.

Tariff Stack Calculation: In the modern environment, the base HTS rate is only the beginning. Managers must account for Section 301, Section 232, Chapter 99 exemptions, and the Merchandise Processing Fee (MPF). SAIL GTX automates this "stack," providing the CFO with the true landed cost of every SKU.

Same-Day Audit Response: By capturing the evidence chain at the time of classification, SAIL GTX allows trade managers to respond to CF-28/29 inquiries on the same day they are received. This 20x improvement in speed directly reduces the likelihood of broader audits and avoids port delays.

Strategic Insights into the 2026 Trade Environment

The 2026 trade landscape is defined by the weaponization of tariffs as a geopolitical tool. Reciprocal tariffs against various trading partners now vary from 10% to 41%, and these are often cumulative with existing executive orders. For example, aluminum and steel imports may be subject to a 50% tariff from most countries but only 25% from the United Kingdom, creating a massive financial incentive and thus a massive enforcement risk regarding the Country of Origin (COO).

The "Reverse False Claim" Risk in 2026

The DOJ is increasingly using the "reverse false claim" theory under the FCA to target companies that should have known they were underpaying. In this environment, "not knowing" is no longer a valid legal defense; it is considered "reckless disregard". The case study proves that even if a company corrects its codes, the failure to pay back-duties is itself a separate violation.

Furthermore, the rise of "qui tam" (whistleblower) lawsuits means that a company’s own employees, consultants, or competitors can file a lawsuit under seal and receive a portion of the recovery. The $22.8 million case settlement and the $4.9 million case settlement were both flagged through whistleblower reports. This internal risk makes the "Confidence Scores" and "Direct Client Collaboration" features of SAIL GTX even more critical for maintaining internal transparency and governance.

Financial ROI of Transitioning to SAIL GTX

For the CFO of a Fortune 500 company, such as the chemicals firm mentioned in the SAIL GTX results, the ROI of AI-native compliance is measured in both direct cost savings and risk mitigation.

Headcount Optimization: By reducing classification time from 45 minutes to 3 minutes, a team can monitor 10,000+ SKUs without adding full-time headcount. This allows the compliance team to shift from manual data entry to "strategic work," such as duty drawback and supply chain optimization.

Audit Avoidance: A 100% catalog review ensures that there are "zero products at risk". The ability to demonstrate "reasonable care" through a documented reasoning chain is the most effective way to prevent a routine CBP inquiry from escalating into a full-scale DOJ investigation.

Margin Protection: Accurate HTS codes ensure that COGS are predicted correctly, preventing the "unpleasant surprises" that occur when back-duties are assessed months after the product has been sold.

The deployment time for SAIL GTX is remarkably short, often achieving full catalog import and calibration within 11 days, compared to the 6+ months typically required for enterprise software implementations. This "time to value" is essential in a trade environment where new tariffs can be implemented via executive order with only a few days of notice.

The Convergence of AI and Trade Governance

The mission of SAIL and its product SAIL GTX is to mitigate the "chaotic communication" and "data verification processes" that are inherent to logistics. By connecting to ERP, WMS, and TMS systems, SAIL GTX bridges the gap between the procurement of a product and its legal entry into the country. The AI-powered "action radar" spotlights urgent issues—such as a missing bill of entry or a mismatched invoice total, before they reach the customs checkpoint.

In the case of complex Bill of Materials (BoM), the AI workspace can find accurate codes even when items have multiple origins, ensuring that valuation and classification are consistent across the entire supply chain. This level of precision is the new standard for "reasonable care" in 2026.

Actionable Recommendations for Finance and Trade Managers

To protect corporate profitability and ensure compliance, the analysis of HTS classification risks suggests several immediate actions:

Conduct a Full Catalog Audit: Move beyond 15% sampling. Use SAIL GTX to review 100% of current HTS codes against the most recent regulatory updates.

Establish a Digital Evidence Chain: Ensure that every classification decision is supported by a reasoning export and a citation from the CROSS database. This documentation should be archived and easily retrievable for at least five years.

Automate Regulatory Alerts: Implement a system that daily monitors the HTS for changes and automatically flags affected products. The "daily reality" of 2,000+ changes makes manual monitoring a mathematical impossibility.

Integrate Compliance into the Financial Close: Treat tariff liabilities with the same rigor as tax liabilities. Use "Tariff Stack Calculators" to ensure that the balance sheet accurately reflects the total landed cost of inventory.

Respond to Audits on the Same Day: Use AI-generated documentation to provide comprehensive, evidence-based responses to CBP inquiries immediately. Speed is a signal of "reasonable care" and operational control.

The financial health of an importing business in 2026 is inextricably linked to the accuracy of its HTS classification. As the cases studies demonstrate, the cost of "getting it wrong" is no longer just a small administrative fee; it is a multi-million dollar liability that can threaten the very viability of the organization. By leveraging the AI-native workspace of SAIL GTX, trade managers can move from a state of "audit dread" to a state of "defensible confidence," ensuring that every classification is a strategic decision rather than a clerical guess.

Ready to transform your Trade Compliance?

See how SAIL can help you classify faster and stay compliant.

Related Articles

100%, 20%, 15%, 0%: Decoding the New U.S. Pharma Tariff Structure

New U.S. pharma tariffs bring rates of 100%, 20%, 15%, and 0%. Here's what's confirmed, what changed, and what to do now.

New Section 301 Tariffs Take Effect: What It Means for Importers

USTR's new Section 301 tariffs (10–12.5%) took effect July 24, 2026 across 60 economies. See country rates and what it means for compliance teams.

The Duty Stack Doesn’t Lie: Using Tariff Layering to Detect Evasion

How HTS classification and full-stack duty analysis reveal what a declared origin cannot hide and why a new Executive Order makes this capability critical.